The trail to a “comfortable touchdown” doesn’t appear as clean because it did 4 months in the past. However the expectations of a yr in the past have been surpassed.

The financial information of the previous two weeks has been sufficient to depart even seasoned observers feeling whipsawed. The unemployment price fell. Inflation rose. The inventory market plunged, then rebounded, then dropped once more.

Take a step again, nonetheless, and the image comes into sharper focus.

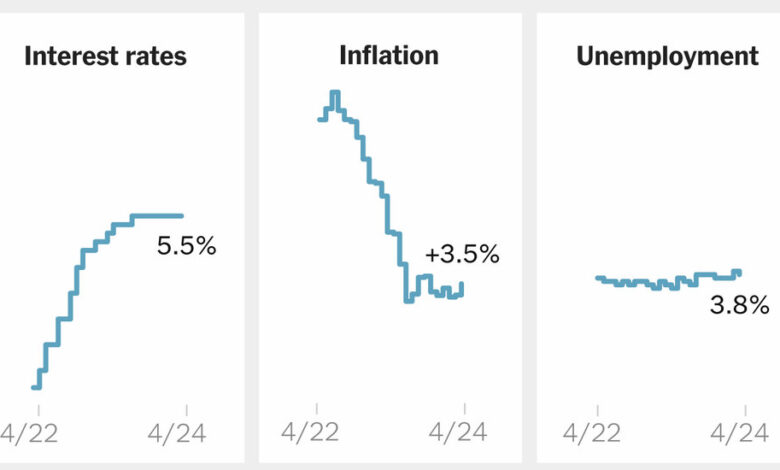

In contrast with the outlook in December, when the economic system gave the impression to be on a glide path to a surprisingly clean “comfortable touchdown,” the current information has been disappointing. Inflation has proved extra cussed than hoped. Rates of interest are prone to keep at their present degree, the very best in many years, not less than into the summer season, if not into subsequent yr.

Shift the comparability level again only a bit, nonetheless, to the start of final yr, and the story adjustments. Again then, forecasters have been extensively predicting a recession, satisfied that the Federal Reserve’s efforts to regulate inflation would inevitably lead to job losses, bankruptcies and foreclosures. And but inflation, even accounting for its current hiccups, has cooled considerably, whereas the remainder of the economic system has up to now escaped important injury.

“It appears churlish to complain about the place we’re proper now,” stated Wendy Edelberg, director of the Hamilton Venture, an financial coverage arm of the Brookings Establishment. “This has been a extremely remarkably painless slowdown given what all of us apprehensive about.”

The month-to-month gyrations in shopper costs, job progress and different indicators matter intensely to traders, for whom each hundredth of a proportion level in Treasury yields can have an effect on billions of {dollars} in trades.

However for just about everybody else, what issues is the considerably longer run. And from that perspective, the financial outlook has shifted in some refined however necessary methods.

Inflation is cussed, not surging.

Inflation, as measured by the 12-month change within the Client Worth Index, peaked at just over 9 percent in the summertime of 2022. The speed then fell sharply for a yr, earlier than stalling out at about 3.5 p.c in current months. Another measure that’s most popular by the Fed reveals decrease inflation — 2.5 p.c within the newest knowledge, from February — however the same general development.

In different phrases: Progress has slowed, nevertheless it hasn’t reversed.

On a month-to-month foundation, inflation has picked up a bit for the reason that finish of final yr. And costs proceed to rise rapidly in particular classes and for particular shoppers. Automobile house owners, for instance, are being hit by a triple whammy of upper fuel costs, increased restore prices and, most notably, increased insurance coverage charges, that are up 22 p.c over the previous yr.

However in lots of different areas, inflation continues to recede. Grocery costs have been flat for 2 months, and are up simply 1.2 p.c over the previous yr. Costs for furnishings, family home equipment and lots of different sturdy items have been falling. Lease will increase have moderated and even reversed in lots of markets, though that has been gradual to indicate up in official inflation knowledge.

“Inflation continues to be too excessive, however inflation is way much less broad than it was in 2022,” stated Ernie Tedeschi, a analysis scholar at Yale Legislation College who lately left a put up within the Biden administration.

The remainder of the economic system is doing nicely.

The current leveling-off in inflation could be a giant concern if it have been accompanied by rising unemployment or different indicators of financial hassle. That will put policymakers in a bind: Attempt to prop up the restoration they usually may danger including extra gas to the inflationary fireplace; hold making an attempt to tamp down inflation they usually may tip the economic system right into a recession.

However that isn’t what is occurring. Exterior of inflation, a lot of the current financial information has been reassuring, if not outright rosy.

The labor market continues to smash expectations. Employers added greater than 300,000 jobs in March, and have added practically three million previously yr. The unemployment price has been beneath 4 p.c for greater than two years, the longest such stretch for the reason that Sixties, and layoffs, regardless of cuts at a number of high-profile firms, stay traditionally low.

Wages are nonetheless rising — not on the breakneck tempo of earlier within the restoration, however at a price that’s nearer to what economists contemplate sustainable and, crucially, that’s sooner than inflation.

Rising earnings have allowed People to maintain spending even because the financial savings they constructed up through the pandemic have dwindled. Eating places and resorts are nonetheless full. Retailers are coming off a record-setting vacation season, and lots of are forecasting progress this yr as nicely. Client spending helped gas an acceleration in general financial progress within the second half of final yr and seems to have continued to develop within the first quarter of 2024, albeit extra slowly.

On the identical time, sectors of the economic system that struggled final yr are displaying indicators of a rebound. Single-family residence building has picked up in current months. Producers are reporting extra new orders, and manufacturing facility building has soared, partly due to federal investments within the semiconductor business.

Rates of interest are going to remain excessive for some time.

So inflation is just too excessive, unemployment is low and progress is stable. With that set of components, the usual policymaking cookbook provides up a easy recipe: excessive rates of interest.

Positive sufficient, Fed officers have signaled that rate of interest cuts, which traders as soon as anticipated early this yr, at the moment are prone to wait not less than till the summer season. Michelle Bowman, a Fed governor, has even suggested that the central financial institution’s subsequent transfer might be to boost charges, not lower them.

Buyers’ expectation of decrease charges was a giant issue within the run-up in inventory costs in late 2023 and early 2024. That rally has misplaced steam because the outlook for price cuts has grown murkier, and additional delays may spell hassle for inventory traders. Main inventory indexes fell sharply on Wednesday after the unexpectedly scorching Client Worth Index report; the S&P 500 ended the week down 1.6 p.c, its worst week of the yr.

Debtors, in the meantime, must anticipate any aid from excessive charges. Mortgage charges fell late final yr in anticipation of price cuts however have since crept again up, exacerbating the present disaster in housing affordability. Rates of interest on bank card and auto loans are on the highest ranges in many years, which is especially laborious on lower-income People, who usually tend to depend on such loans.

There are indicators that increased borrowing prices are starting to take a toll: Delinquency charges have risen, significantly for youthful debtors.

“There are causes to be apprehensive,” stated Karen Dynan, a Harvard economist who was a Treasury official beneath President Barack Obama. “We are able to see that there are components of the inhabitants which are for one motive or one other coming beneath pressure.”

Within the mixture, nonetheless, the economic system has withstood the cruel medication of upper charges. Client bankruptcies and foreclosures haven’t soared. Nor have enterprise failures. The monetary system hasn’t buckled as some folks feared.

“What ought to hold us up at evening is that if we see the economic system slowing however the inflation numbers not slowing,” Ms. Edelberg of the Hamilton Venture stated. Up to now, although, that isn’t what has occurred. “We nonetheless simply have actually sturdy demand, and we simply want financial coverage to remain tighter for longer.”